Exactly where on the income statement "Income (Loss) from Equity Method Investments" is reported.

Whether "Operating Income (Loss)" is reported on the income statement.

Whether "Exchange Gains (Losses) from Foriegn Currency Trasnactions" is reported as part of net cash flow or as part of the roll forward of cash and cash equivalents.

The FASB in SFAC 8 makes the following statements about comparability:

QC20. Users' decisions involve choosing between alternatives, for example, selling or holding an investment, or investing in one reporting entity or another. Consequently, information about a reporting entity is more useful if it can be compared with similar information about other entities and with similar information about the same entity for another period or another date.

QC21. Comparability is the qualitative characteristic that enables users to identify and understand similarities in, and differences among, items. Unlike the other qualitative characteristics, comparability does not relate to a single item. A comparison requires at least two items.

QC22. Consistency, although related to comparability, is not the same. Consistency refers to the use of the same methods for the same items, either from period to period within a reporting entity or in a single period across entities. Comparability is the goal; consistency helps to achieve that goal.

QC23. Comparability is not uniformity. For information to be comparable, like things must look alike and different things must look different. Comparability of financial information is not enhanced by making unlike things look alike any more than it is enhanced by making like things look different.

QC24. Some degree of comparability is likely to be attained by satisfying the fundamental qualitative characteristics. A faithful representation of a relevant economic phenomenon should naturally possess some degree of comparability with a faithful representation of a similar relevant economic phenomenon by another reporting entity.

QC25. Although a single economic phenomenon can be faithfully represented in multiple ways, permitting alternative accounting methods for the same economic phenomenon diminishes comparability.

As the conceptual framework points out "comparibility is NOT uniformaty". What makes US GAAP such a robust reporting scheme is that it strikes an appropriate equilibrium between uniformity and flexibility. This does not

mean that financial reports can be "random". The judgement of a professional accountant is used, that judgement helps economic entities reach a sensible conclusion about how information is reported.

So although financial statements are not "uniform" or "forms", they DO HAVE recognizable patterns. These prototype tools can help you see these patterns:

Income statements have the most variability; the other statements tend to be much more comparible.

The next section starts to dig deeper into two specific reporting styles and tries to "map" between the two styles so specific issues related to comparing across different reporting styles can be understood.

Reporting style: Commercial and Industrial Company, Gross Profit, Operating Income (Loss)

This reporting style is used by approximately 1,579 public companies. If you go to this web page you can see the specifics of this reporting style.

On the LEFT is the income statement from one company that reports using this style. On the RIGHT is the standardized "pattern" of the report elements for this reporting style.

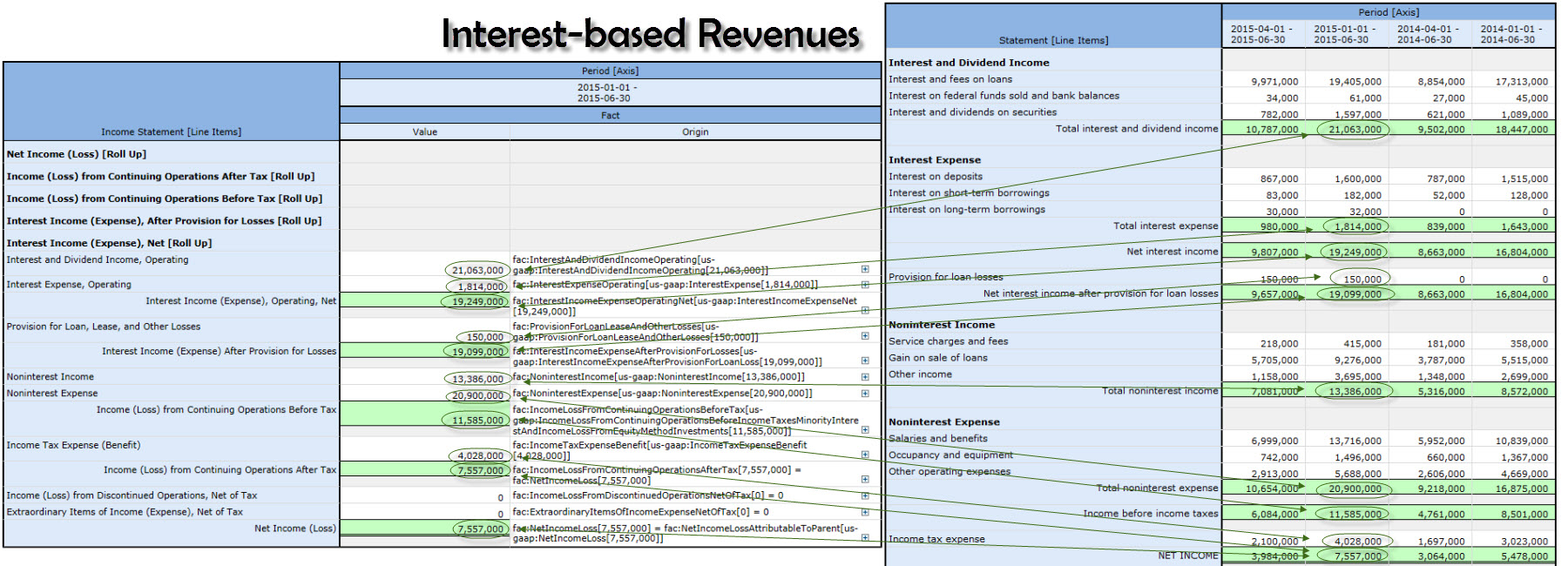

Reporting style: Interest-based Revenues

This reporting style is used by approximately 535 public companies, generally depository institutions (i.e. banks). If you go to this web page you can see the specifics of this reporting style.

On the RIGHT is the income statement from one company that reports using this style. On the LEFT is the standardized "pattern" of the report elements for this reporting style.

Reporting style: Mapping Between the Two

This graphic shows BOTH standard reporting patterns; one on the left and the other on the right; and tries to "map" one style to the other style. This is what is necessary in order to effectively compare economic entities that use different reporting styles.

Conclusions

And so, the following information is helpful in understanding the comparibility of XBRL-based public company financial reports.

Financial reports are not "uniform". Such reoprts are not forms. However, there are patterns that exist in reported information and those patterns can be used to compare financial reports.

Period-to-period comparisons for one economic entity are generally not an issue because such economic entities are required to create financial reports consistently from one period to another. They can make changes, but there are rules that govern such reporting changes. Such changes are not arbitrary.

Comparibility across economic entities that use the same reporting style are generally straight forward.

Comparibility across economic entities that use different reporting styles is possible, exactly how to do these comparisons involves personal preferences and judgement.

Key to creating comparinsons between different reporting styles involves distilling the pieces that make up a financial report component.

The FASB defines nine fundamental elements of a financial report; while that set is helpful, it is not sufficient for comparing across economic entities. Standard defintions for these terms are necessary: (this is not a complete set but rather just examples, precise definitions for these terms is critical)

Balance sheet: Assets, Current Assets, Noncurrent Assets, Fixed Assets, Capitalization, Liabilities, Equity, Temporary Equity, Redeemable Noncontrolling Interest, Equity Attributable to Parent, Equity Attributable to Noncontrolling Interests

Income statement: Revenues (operating), Nonoperating revenues, Cost of Revenues, Operating Expenses, Costs and Expenses (operating), Costs and Expenses (Operating and Nonoperating), Gross Profit, Operating Income (Loss), Other Operating Income, Nonoperating Income (Losses), Income from Continuing Operations Before Tax, Income Tax Expense (Benefit), Income (Loss) from Equity Method Investments, Net Income (Loss), Net Income (Loss) Attributable to Parent, Net Income (Loss) Attributable to Noncontrolling Interest, Preferred Dividends and Other Adjustments, Net Income (Loss) Available to Common Stockholders

Cash Flow Statement: Net Cash Flow, Net Cash Flow from Operating Activities, Net Cash Flow from Investing Activites, Net Cash Flow from Financing Activities, Net Cash Flow, Continuing Operations, Net Cash Flow, Discontinued Operations, Exchange Gains (Losses) on Foriegn Currency Transactions, Net Cash Flow Related to Assets Held-for Sale

Comprehensive Income: Net Income (Loss), Other Comprehensive Income, Comprehensive Income

Key Ratios: Return on Equity, Return on Assets, Return on Sales, Sustainable Growth Rate, Working Capital, Debt/Equity Ratio

All of this information should be provide in machine-readable form.

Based on evidence from XBRL-based public company financial filings to the SEC, 90% of all public companies fit into one of 80 different reporting styles. It is estimated that 100% of public companies would fit into less than 250 different reporting styles (perhaps less).

It is possible for an economic entity to have a reporting style that is unique to that one entity. (i.e. a set of reporting styles could have only one member, but every public company can be said to have some reporting style.)

Understanding what you are comparing is critical. Thinking that you are comparing similar line items because they are labeled the same, but the meaning is truly different should be avoided.